NVDA Acquires Groq; Semis Shed 6% on Iran, H200 China Overhang

- May 19

- 1 min read

AI infrastructure is no longer just a technology buildout. It is becoming a capital structure question.

Aggregate hyperscale capex has crossed above free cash flow. At the same time, physical constraints around power, memory, and compute are becoming visible across the stack.

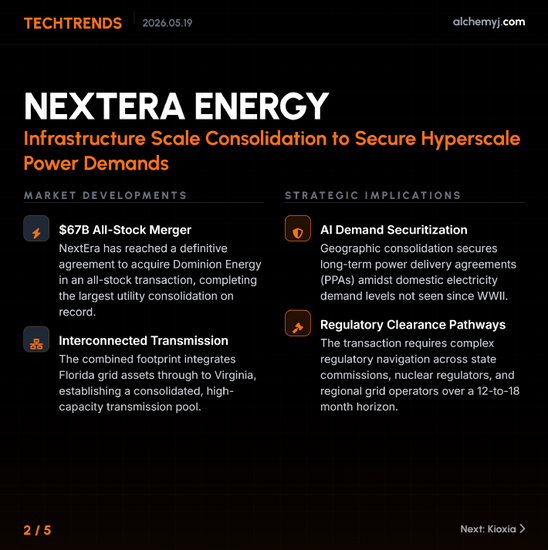

Recent utility consolidation and stronger memory pricing signals are not isolated developments. They point to the same pressure surfacing in different layers of the AI infrastructure system.

That is where the analytical work now sits.

A portfolio may appear to have broad “AI exposure,” but that exposure can sit in very different parts of the stack — infrastructure, compute, energy and grid capacity, hardware supply, or the instruments used to hedge cost volatility.

Each layer carries a different margin profile, financing structure, and return horizon.

The question is not whether the buildout continues. It is whether the framework used to evaluate AI exposure can distinguish where the capital is deployed, where the risk is financed, and where the return is captured.

For investors, “AI exposure” is no longer a single category.

The harder question is whether the valuation framework can separate where capital is being spent from where returns may ultimately accrue.

Follow us on LinkedIn or subscribe to “FinTech Insights” for more information about FinTech.

Disclaimer: This article is for informational purposes only and is not investment or professional advice. Information and views are from public sources we believe to be reliable, but we do not guarantee their accuracy or completeness. Content is subject to change. Readers should exercise their own judgment and consult a professional advisor. Any action taken is at your own risk.

Copyright © 2026 Axisoft. All Rights Reserved